%201.png)

A curated list of essential terms in private market secondaries, covering pricing, valuation, deal structure, and investment strategies. Designed for brokers, investors, and analysts navigating the pre-IPO and late-stage private markets.

Valuation & Pricing

409A Valuation

- An independent appraisal of the fair market value of a private company’s common stock.

Scenario:

A fast-growing SaaS startup is preparing to issue stock options to new hires. To comply with IRS regulations and avoid tax penalties, the company engages a valuation firm to conduct a 409A valuation, determining the fair market value of its common shares.

Why This Matters:

Ensures tax compliance, avoids penalties, supports fair option pricing, attracts and retains talent, provides defensible valuations.

The Process:

The company’s finance team gathers financials, cap table, and recent transaction data. The valuation firm analyzes market comps, financial projections, and applies appropriate valuation methodologies (e.g., DCF, market approach). The final report is delivered to the board and used to set option strike prices.

Fair Value/Fair Market Value

- The estimated price at which an asset would trade between willing parties in an open market, often used in financial reporting and valuation.

Scenario:

A private equity fund must report the fair value of its portfolio companies to LPs each quarter, using market comps and discounted cash flow analysis.

Why This Matters:

Ensures transparency, regulatory compliance, impacts performance metrics, supports exits and secondary sales.

The Process:

Valuation teams document methodologies, assumptions, and reconcile with third-party appraisals as needed.

Valuation Services

- Professional services that determine the value of a company, security, or asset, often for investment, tax, or financial reporting purposes.

Scenario:

A private equity firm hires a third-party provider for valuation services to support quarterly reporting and fundraising.

Why This Matters:

Enhances credibility, supports compliance, reduces conflicts, improves transparency.

The Process:

The provider reviews financials, market comps, and applies industry-standard methodologies, delivering detailed valuation reports.

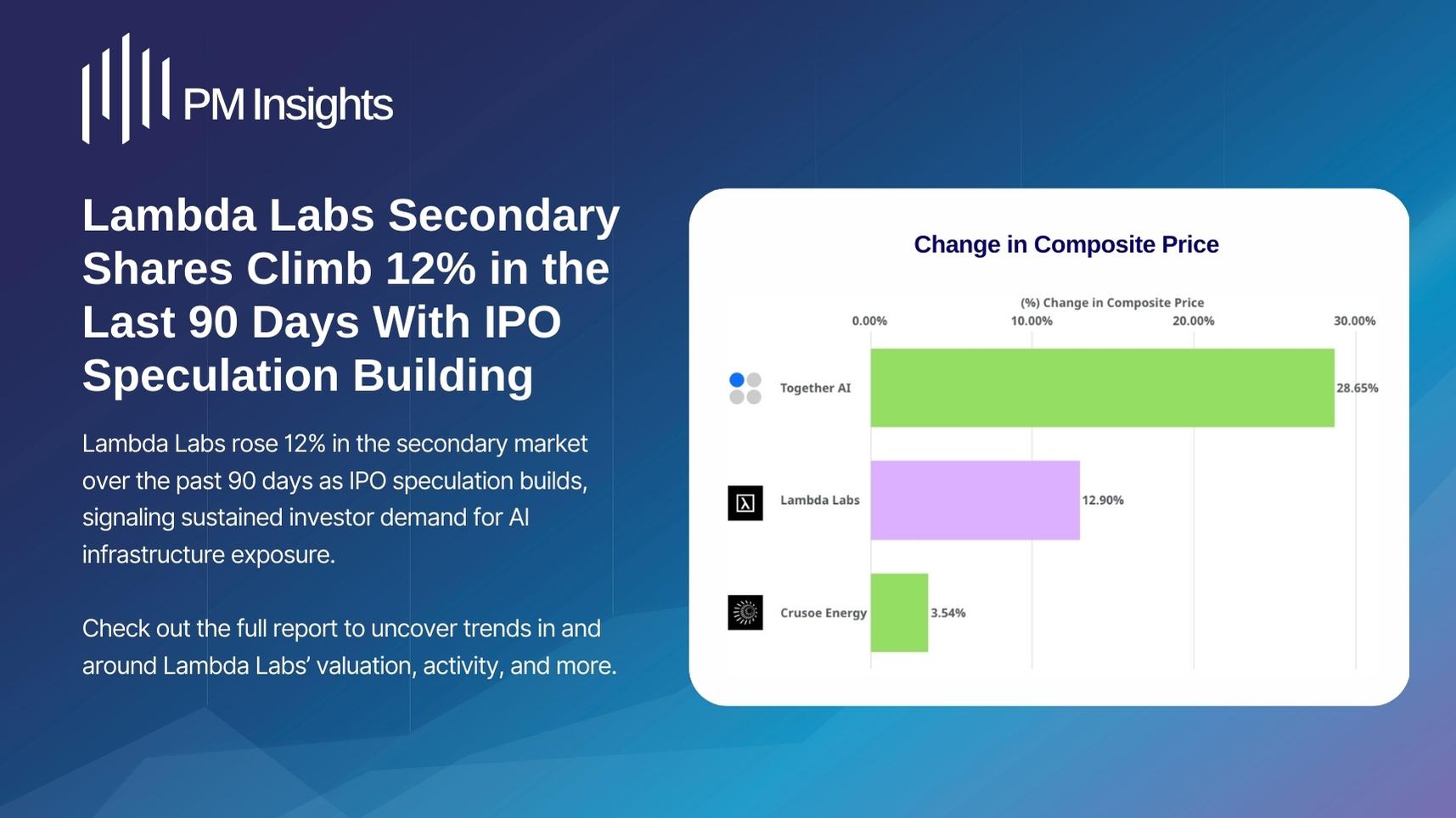

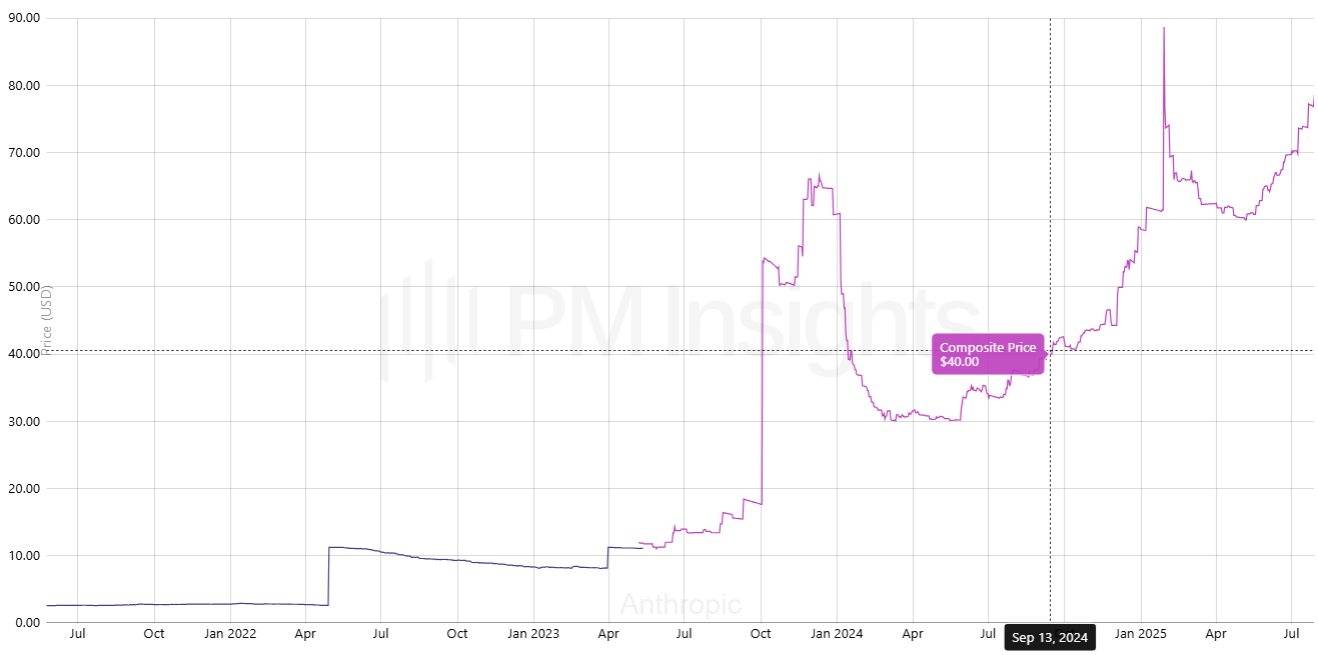

Composite Price

- An aggregated price derived from multiple sources or trades, providing a representative value for illiquid or thinly traded securities.

Scenario:

A private equity fund is valuing a portfolio company for quarterly reporting. It uses a composite price derived from multiple data sources, including recent transactions and market comps.

Why This Matters:

Provides accurate, market-reflective valuation, supports fair value reporting, increases transparency, reduces bias.

The Process:

Valuation teams aggregate prices from different sources, apply weighting, and document the methodology.

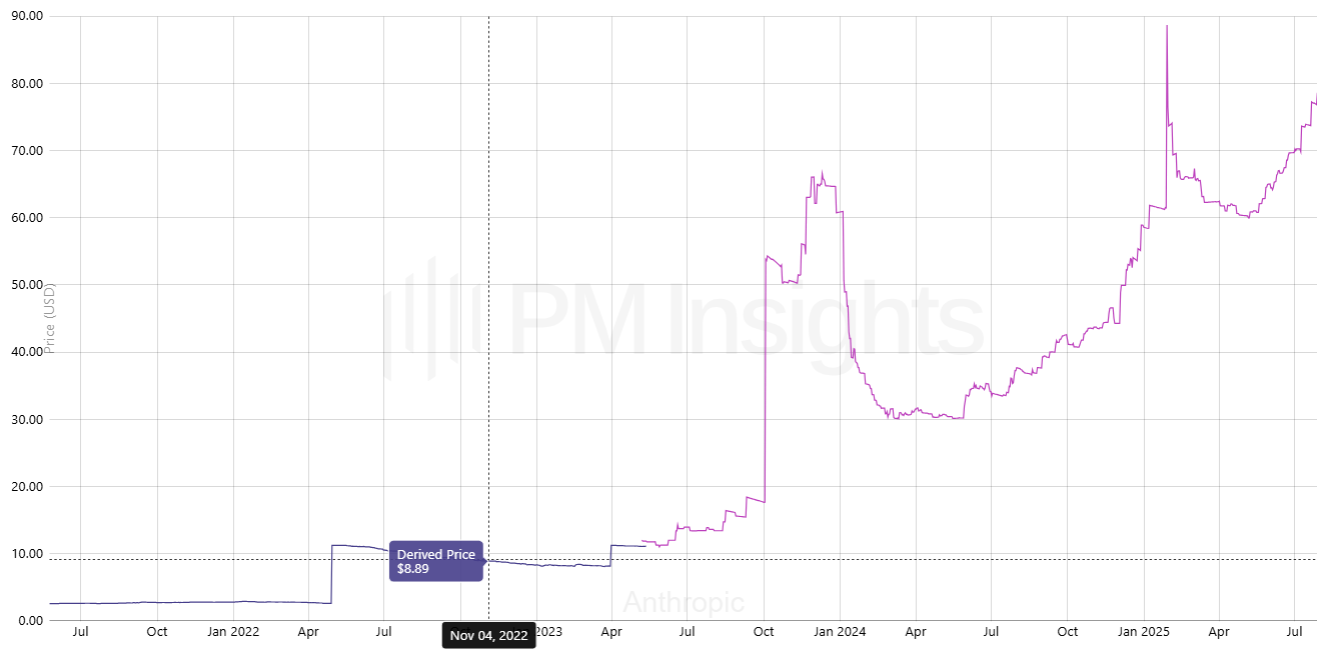

Derived Price

- A calculated estimate of a security’s value based on market data or pricing models.

Scenario:

A secondary market platform lists shares of a unicorn startup. The derived price is calculated using recent secondary trades, implied valuations, and investor demand.

Why This Matters:

Provides reference for buyers and sellers, aids fair value estimation, informs negotiation and pricing.

The Process:

The platform aggregates data, applies statistical models, and publishes a derived price for market participants.

Jump-Off Point

- A recent transaction or valuation used as a reference for estimating a company's current value, particularly in secondary market analysis.

Scenario:

A late-stage VC fund identifies a “jump off point” where a portfolio company’s growth accelerates, justifying a higher valuation and potential exit.

Why This Matters:

Maximizes returns, identifies inflection points, guides exit timing and value creation strategy.

The Process:

The team tracks KPIs, market traction, and competitive dynamics to anticipate the optimal exit window.

Investment Types & Strategies

Alternative Investments

- Non-traditional assets outside public stocks, bonds, or cash. This category includes private equity, venture capital, hedge funds, private credit, real assets, and collectibles, often offering portfolio diversification and higher return potential.

Scenario:

A family office with a $200 million portfolio seeks to reduce public market exposure and improve risk-adjusted returns. It allocates $30 million to alternative investments, including hedge funds, private equity, and real assets.

Why This Matters:

Offers diversification, potential for higher returns, lower correlation with public markets, access to unique strategies, alpha generation.

The Process:

The CIO screens managers, reviews historical performance, and assesses fit with the family’s risk profile. Allocations are made via limited partnerships or direct investments, with ongoing monitoring of performance and liquidity.

Venture Capital

- A type of private equity investment focused on early-stage companies with high growth potential, often in exchange for equity.

Scenario:

A university endowment allocates $100 million to venture capital funds focused on early-stage AI and robotics startups.

Why This Matters:

Access to innovation, high-growth opportunities, diversifies portfolio, potential for outsized returns.

The Process:

The investment office screens VC managers, reviews track records, and negotiates fund terms, with ongoing monitoring of portfolio progress.

Late Stage Investing

- Investments made in mature private companies with proven business models, typically close to an IPO or acquisition.

Scenario:

A sovereign wealth fund allocates $500 million to late-stage venture funds targeting pre-IPO tech companies.

Why This Matters:

Lower risk, faster liquidity, access to mature high-growth companies, potential for outsized returns.

The Process:

The fund selects managers with strong networks, evaluates pipeline companies, and negotiates terms for preferred shares.

Pre-IPO

- Refers to a private company in the stage immediately preceding its initial public offering. Investments during this phase are often made by institutional or accredited investors.

Scenario:

A hedge fund participates in a pre-IPO round for a high-profile biotech firm, seeking to capture upside before the public listing.

Why This Matters:

Access to IPO pop, invest at a discount, enhances returns, diversifies portfolio.

The Process:

The fund negotiates allocation, reviews lock-up terms, and models exit scenarios post-IPO.

Company Structure & Ownership

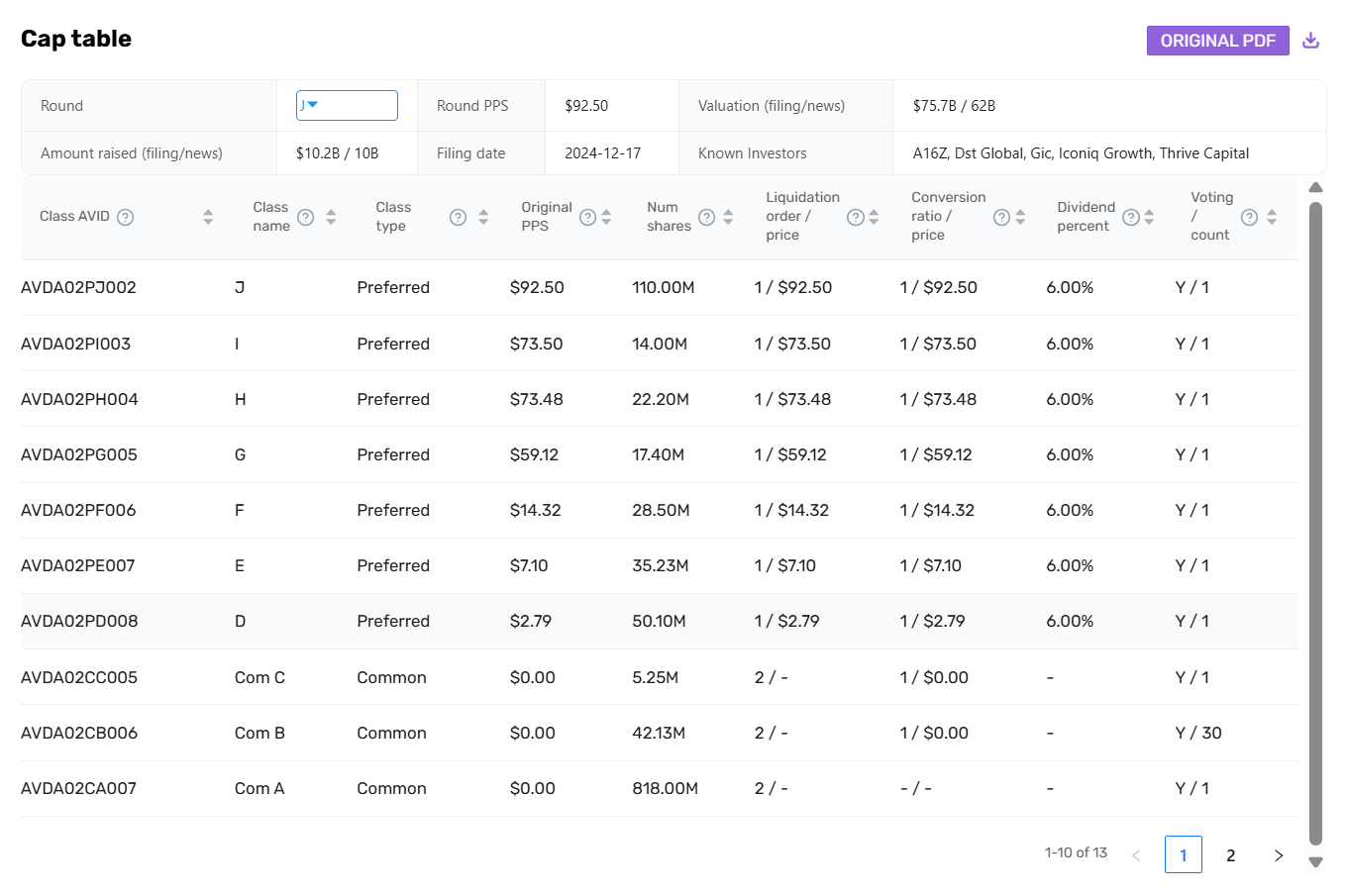

Cap Tables

- Spreadsheets that detail the ownership structure of a company, including equity stakes, options, and convertible securities.

Scenario:

A venture-backed startup is raising a Series C round. The VC firm reviews the company’s cap table to assess dilution and investor rights.

Why This Matters:

Shows ownership, option pools, liquidation preferences, helps understand dilution, control, and exit outcomes.

The Process:

The VC’s analysts model post-money ownership and potential outcomes under various exit scenarios.

Special Purpose Vehicle (SPV) https://www.pminsights.com/spv-calculator

- A legal entity created to isolate investment risk, often used to pool capital from investors into a single target investment.

Scenario:

An angel syndicate pools capital from multiple investors into an SPV to invest in a single high-growth startup.

Why This Matters:

Enables collective investment, limits liability, simplifies cap table, provides access to larger deals.

The Process:

A lead investor sets up the SPV, manages legal and compliance, and allocates returns pro rata.

Unicorn

- A privately held startup company valued at over $1 billion, typically backed by venture capital and considered to have high growth potential.

Scenario:

A growth equity fund targets investments in unicorns—private companies valued at over $1 billion—seeking rapid value appreciation.

Why This Matters:

Potential for significant gains, attracts LPs and media, may provide liquidity via secondary sales or IPOs.

The Process:

The fund screens for unicorns with strong fundamentals and exit potential, negotiating terms for minority stakes.

Trading & Execution

Best Execution

- The obligation to execute client orders in a way that ensures the most favorable terms reasonably available across price, speed, and likelihood of execution.

Scenario:

An asset manager trading large blocks of equities for a pension fund seeks best execution to minimize transaction costs and market impact.

Why This Matters:

Reduces trading costs, preserves returns, meets fiduciary duty, enhances client trust, meets regulatory standards.

The Process:

Traders use algorithms, smart order routing, and multiple venues to achieve optimal price and liquidity. Post-trade analysis reviews execution quality.

Bid-Ask

- The spread between the highest price a buyer is willing to pay (bid) and the lowest price a seller will accept (ask) for a security. A key measure of market liquidity.

Scenario:

A hedge fund is considering buying a block of illiquid private company shares on a secondary market. The bid-ask spread is wide due to low trading volume.

Why This Matters:

Wide spreads increase costs, reduce liquidity, signal market uncertainty, impact pricing and portfolio valuation.

The Process:

Negotiations with the seller may narrow the spread. The fund evaluates whether the expected return justifies the cost.

Deal on Desk

- A live investment opportunity currently being evaluated or processed by an investment team.

Scenario:

A growth equity investor receives a confidential information memorandum for a promising fintech startup. The deal is now “on desk” and under active review.

Why This Matters:

Early access secures favorable terms, creates competitive advantage, supports deal flow management.

The Process:

The investment team conducts initial screening, diligence, and internal discussions before deciding to proceed.

Risk Management

Downside Risk

- The potential loss in value of an investment in a worst-case scenario, often used to assess risk-adjusted returns.

Scenario:

A pension fund considers investing in a private infrastructure project. The team models downside risk scenarios, including regulatory changes and demand shocks.

Why This Matters:

Protects against capital loss, informs portfolio construction, supports prudent risk management, meets fiduciary duty.

The Process:

Risk teams use scenario analysis, stress testing, and sensitivity analysis to quantify potential losses.

Duration Risk

- The risk that changes in interest rates will negatively impact the value of an investment, particularly fixed-income securities with longer maturities.

Scenario:

A private credit fund invests in long-term loans to renewable energy projects. Rising interest rates increase duration risk, potentially eroding returns.

Why This Matters:

Affects asset values and income, important for liability matching, impacts interest rate exposure and hedging.

The Process:

The fund uses interest rate swaps and duration matching to mitigate risk.

Market Data & Analytics

Private Market Data

- Information and analytics related to pricing, valuation, and performance of private market investments.

Scenario:

A fund-of-funds manager uses private market data providers to benchmark returns and valuations of underlying VC and PE funds.

Why This Matters:

Improves decision-making, enables benchmarking, supports diligence and risk management.

The Process:

The manager subscribes to data platforms, integrates feeds into analytics, and reviews trends for portfolio optimization.

Double Blind Intro

- A confidential introduction where neither party knows the other's identity until both agree to proceed, often used to protect sensitive investment relationships.

Scenario:

A VC syndicate wants to introduce a portfolio company to a strategic acquirer without revealing identities until mutual interest is confirmed.

Why This Matters:

Protects confidentiality, reduces reputational risk, facilitates open discussions, preserves competitive intelligence.

The Process:

An intermediary facilitates the introduction, sharing anonymized profiles until both parties agree to proceed.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)